If you select a policy that includes inflation defense as a basic policy term, you will not need to pay a greater premium for it. In any case, ensure the policy includes it. The best types of inflation protection include: Compounding automated boost, which automatically increases advantages yearly and https://www.canceltimeshares.com/blog/why-is-it-so-hard-to-cancel-a-timeshare/ uses the increased benefit quantity as the base for determining the next year's increase. Simple automatic boost, which immediately increases advantages each year however uses the policy's initial benefit amount to determine the increase. Included protection purchase, which increases advantages every couple of years however at an additional cost. The effectiveness of the inflation security advantage is closely connected to making sure the day-to-day https://www.timesharetales.com/blog/why-is-it-so-hard-to-cancel-a-timeshare/ advantage is as high as possible.

When it comes to older individuals and money, fraud is something to keep an eye out for. If the sales pitch sounds too good to be true, it probably is. Constantly inspect the insurance provider's rating and complaint history with your state insurance commissioner before signing any contracts or making any payments. If a company has a consistent pattern of grievances or a poor performance history of honoring claims, select a different business (How much is dental insurance). Your enjoyed one isn't likely to gather on their policy for numerous years. If the company that provided the policy goes out of company in the interim, they'll be left holding a really expensive however potentially worthless paper.

An insurance company's monetary strength ranking is likewise the very best indication of its ability to pay out on advantage claims. The insurance provider decides when to pay advantages based upon eligibility described as benefit triggers. Some states require particular advantage sets off, however tax-qualified policies generally have the very same triggers no matter where the policy is bought. Typically, advantages are activated by: When the insurance policy holder is unable to perform a particular variety of ADLs, usually two or 3, they become eligible for advantages. Some policies define that just specific ADLs certify, however others allow the policyholder to use any of the fundamental ADLs as triggers.

Some Ideas on What Does Flood Insurance Cover You Need To Know

Nevertheless, some policies will not pay advantages for cognitive problems if the insurance policy holder can still carry out ADLs on their own. A lot of states no longer enable insurer to limit benefits because the policyholder just experiences Alzheimer's. This is sometimes the only method a policy will begin paying benefits and requires the insurance policy holder's medical professional to license that long-term care is clinically needed. How does insurance work. Since your liked one can't trigger benefits without this certification, it's finest to prevent these policies. Insurance coverage companies that supply tax-qualified policies aren't enabled to use this advantage trigger. A long-term care insurance plan pays advantages either on a per diem basis (a fixed benefit no matter the costs for care) or an indemnity basis (a portion of the actual costs of care is repaid to the policyholder).

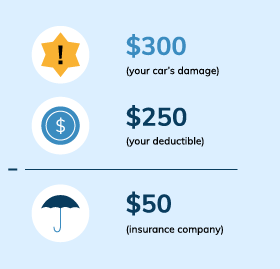

The majority of policies include a deductible or waiting duration prior to coverage begins, especially if the insurance policy holder has any pre-existing conditions. Normally, this is described an removal period, and it indicates advantages will not start the very first day the insurance policy holder gets in a long-term care center or begins utilizing home care. Removal periods can be between no and 100 days but are often 30, 60 or 90 days and may differ for retirement home care versus house care. Throughout this duration, policyholders should cover the cost of their care themselves. Choose a policy that only requires the policyholder to satisfy their removal duration when, rather of making them wait each time a new need for care occurs. How does insurance work.

Some policies specify this maximum in a dollar amount however most specify it in years. In a lot of states, the minimum advantage limit is one year, but you can purchase a policy that consists of any variety of years. You might even have the ability to acquire a policy that lasts as long as you need care, however "life time" policies are almost nonexistent today. If cost is among the concerns keeping your parents or other loved ones from buying a long-term care insurance plan, consider the tax advantages that support them. If your enjoyed one gets a tax-qualified policy, they can detail the premiums, together with their other medical expenses.

3 Simple Techniques For How Much Does Long Term Care Insurance Cost 2021

5 percent of the insurance policy holder's adjusted gross earnings can be used as a reduction. Few people receive a complete deduction on their premium; nevertheless, if they own a health cost savings account, they might be able to subtract more. Tax benefits increase sharply for self-employed individuals. Instead of making a list of premiums, they declare the entire quantity as a self-employed health insurance coverage reduction, which comes off the top of their income. They do not even have to be self-employed full-time to take advantage of this deduction. If your enjoyed one owns or comes from a C corporation, they can state the whole premium as tax deductible.

For example, numerous self-employed persons in the 30 percent tax bracket might be able to save 20 percent or more of their premiums in tax benefits. Always seek advice from an accounting professional or tax lawyer to discover which tax benefits specifically use to your loved one's scenario. If your enjoyed one never requires or gets approved for their long-term care insurance coverage advantages or they collect benefits for only a brief time, the years of paying premiums might appear like a squandered investment. Nevertheless, if they wind up needing look after an extended quantity of time, the money was certainly well invested. Oftentimes, a long-term care policy is more of a "comfort" financial investment than a sound financial one.

Individuals guarantee their lives, homes and lorries to prevent getting knocked by financial challenge needs to something unforeseen take place. Shouldn't the exact same precautions be made with a person's future health? Choosing whether to purchase long-lasting care insurance is a hard decision, but here are a couple of powerful positives people might overlook: Having a long-term care policy in place helps relieve and even prevent all types of tension on caretakers, so aging grownups need not fear becoming a problem to their household. If you have aging parents or other loved ones who do not live nearby, you may stress who will provide take care of them should they no longer be able to care for themselves.

The Main Principles Of How Much Is Pet Insurance

Long-lasting care insurance can reduce these concerns by offering the necessary resources to put them in control of the place, type and quality of care they get. The high cost of long-term healthcare can quickly diminish even a healthy nest egg. It could even need the liquidation of assets, such as a house. This puts a financial challenge on a healthy partner and the children. Long-lasting care insurance supplies the methods to get medical assistance without using savings, which protects member of the family from financial distress. The ever-increasing expense of long-term care insurance coverage and uncertainty over the qualification process makes lots of Americans leery of purchasing an item they often understand little about.